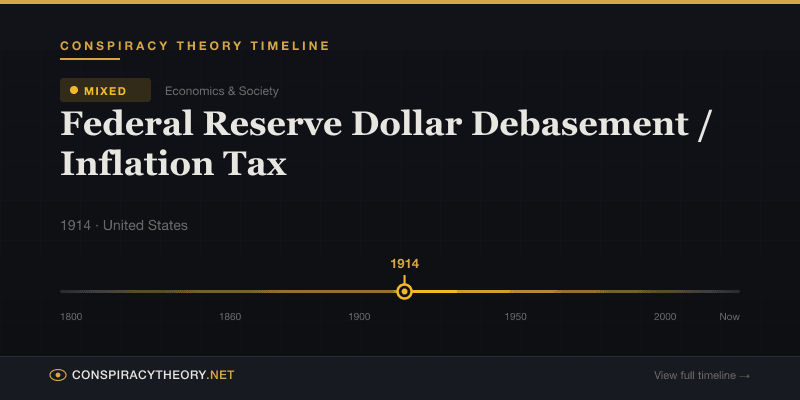

Federal Reserve Dollar Debasement / Inflation Tax

Overview

A dollar in 1913 — the year the Federal Reserve opened its doors — is worth about three cents today. That is not a conspiracy theory. It is the Bureau of Labor Statistics’ own math, available to anyone with an internet connection and a CPI calculator. The U.S. dollar has lost approximately 97% of its purchasing power since a cabal of bankers and one senator met on a private island off the coast of Georgia to design the institution that would control America’s money supply.

If you think that sentence sounds like the opening of a thriller, you are not alone. The Federal Reserve’s origin story is one of the few episodes in American financial history that actually lives up to the conspiracy narrative: secret meetings, powerful men traveling under pseudonyms, a legislative maneuver pushed through during Christmas recess. The facts are dramatic enough that they have sustained more than a century of theories about the Fed’s true purpose — some of them reasonable, some of them unhinged, and some of them disturbingly well-supported by the data.

The dollar debasement theory, in its simplest form, argues that the Federal Reserve systematically destroys the purchasing power of the currency through money creation, functioning as a hidden tax that transfers wealth upward — from savers and wage earners to asset holders, banks, and the federal government itself. In its more extreme versions, it holds that this is not a side effect of policy but its explicit purpose: that the Fed was designed by bankers, for bankers, to ensure a permanent flow of wealth from the many to the few.

What makes this theory fascinating — and what separates it from most entries in a conspiracy encyclopedia — is how much of it is simply mainstream economics described in unflattering terms.

Origins & History

Jekyll Island: The Meeting That Actually Happened

In November 1910, Senator Nelson Aldrich of Rhode Island — the most powerful man in the U.S. Senate and, not coincidentally, the father-in-law of John D. Rockefeller Jr. — organized a secret gathering at the Jekyll Island Club, an exclusive hunting retreat off the Georgia coast. The attendees traveled in a private railcar and used only first names to avoid being identified. They included:

- Frank Vanderlip, president of National City Bank (now Citibank)

- Henry P. Davison, senior partner at J.P. Morgan & Company

- Charles D. Norton, president of the First National Bank of New York

- Benjamin Strong, representing J.P. Morgan

- Paul Warburg, partner at Kuhn, Loeb & Company and an expert in European central banking

- A. Piatt Andrew, Assistant Secretary of the Treasury

This meeting was not a rumor. Frank Vanderlip confirmed it in a 1935 article in The Saturday Evening Post: “There was an occasion, near the close of 1910, when I was as secretive — indeed as furtive — as any conspirator… I do not feel it is any exaggeration to speak of our secret expedition to Jekyll Island as the occasion of the actual conception of what eventually became the Federal Reserve System.”

The group spent roughly ten days drafting what became the Aldrich Plan — the legislative framework for a central bank. After political revisions (the bill was reworked under the direction of Virginia Representative Carter Glass and renamed to distance it from Aldrich’s Wall Street associations), it was signed into law by President Woodrow Wilson on December 23, 1913.

Critics have long noted the timing: the vote occurred two days before Christmas, when many members of Congress had already left Washington. Supporters counter that the bill had been debated for months and the timing was incidental. Both claims have some merit.

The Gold Standard Era and Its Unraveling

For its first decades, the Federal Reserve operated within the constraints of the gold standard. Dollars were redeemable for gold, which limited how much money the Fed could create. This arrangement began eroding during the Great Depression, when Franklin Roosevelt issued Executive Order 6102 in 1933, requiring citizens to surrender their gold holdings at $20.67 per ounce. He then revalued gold to $35 per ounce — an overnight devaluation of the dollar by roughly 41%.

The Bretton Woods system (1944-1971) maintained a modified gold standard in which foreign governments could redeem dollars for gold, but American citizens could not. This arrangement collapsed on August 15, 1971, when Richard Nixon “temporarily” suspended gold convertibility — a temporary measure that is now in its sixth decade. The dollar became a pure fiat currency: money backed by nothing except the government’s promise and the Fed’s management.

For critics of the Fed, the Nixon Shock was the moment the guardrails came off. Without gold convertibility, there was no external limit on how many dollars the Fed could create. And create them it did.

Quantitative Easing and the Post-2008 Explosion

The 2008 financial crisis marked a new chapter. Under Chairman Ben Bernanke — a scholar of the Great Depression who believed the Fed’s great error in the 1930s was not creating enough money — the Fed launched quantitative easing (QE), a program of large-scale asset purchases. The Fed’s balance sheet expanded from roughly $900 billion in 2008 to $4.5 trillion by 2015. Then came COVID-19, and the balance sheet nearly doubled again, peaking near $9 trillion in 2022.

In plain English: the Federal Reserve created trillions of dollars and used them to buy Treasury bonds and mortgage-backed securities from banks and financial institutions. The stated purpose was to lower interest rates, stimulate lending, and prevent economic collapse. The observed effect, critics note, was also to inflate asset prices — stocks, bonds, real estate — while wage growth remained sluggish. Between 2009 and 2019, the S&P 500 quadrupled. Median household income, adjusted for inflation, grew by about 8%.

Thomas Hoenig, president of the Federal Reserve Bank of Kansas City and the lone dissenter against QE in 2010, later put it bluntly: “We have a system that is exacerbating wealth inequality. The people who are most able to take advantage of low interest rates are those who already have assets.”

Key Claims

-

The dollar’s decline is deliberate, not accidental. The Fed targets approximately 2% annual inflation as explicit policy. Over decades, this compounds into massive purchasing power loss. Critics argue that a policy designed to produce inflation is, by definition, a policy designed to debase the currency — the debate is whether this is prudent management or legalized theft.

-

Inflation is a hidden tax that transfers wealth upward. When new money is created, the first recipients (banks and financial institutions) benefit most because they spend it before prices adjust. By the time it reaches ordinary consumers, prices have already risen. This is known as the Cantillon Effect, named after 18th-century economist Richard Cantillon, and it is not disputed by mainstream economics — only its significance is debated.

-

The Fed was designed by bankers to serve banking interests. The Jekyll Island meeting is historical fact. The Fed’s structure — a network of regional banks owned by member commercial banks, with a board appointed by the president but operationally independent — gives the banking sector structural influence over monetary policy that no other industry enjoys.

-

Quantitative easing was a bailout of Wall Street disguised as economic stimulus. The $4.5 trillion in post-2008 QE went to financial institutions, inflating asset prices and generating record profits for banks while the real economy experienced the weakest recovery since World War II.

-

The Federal Reserve operates without meaningful oversight. The Fed has never had a full, independent audit. The Government Accountability Office is prohibited by law from auditing monetary policy decisions, transactions with foreign governments, and deliberations of the Federal Open Market Committee. Ron Paul’s “Audit the Fed” bills passed the House repeatedly but never became law.

Evidence & Analysis

What Is Documented Fact

The dollar’s purchasing power decline is not in dispute. The Bureau of Labor Statistics, the Fed’s own data, and every mainstream economics textbook confirm it. The Fed’s 2% inflation target is publicly stated policy.

The Cantillon Effect — that money creation benefits first recipients disproportionately — is an established concept in economics. The distributional consequences of QE have been acknowledged by Fed officials themselves. A 2012 Bank of England report found that its own QE program had “ichly benefited” the wealthiest 5% of households.

The revolving door between the Fed, Wall Street, and the Treasury Department is documented. Former Goldman Sachs executives have held positions including Treasury Secretary (Robert Rubin, Hank Paulson), Fed president (William Dudley at the New York Fed), and numerous advisory roles. This is public record.

The Jekyll Island meeting, the secrecy, and the participants are all confirmed by primary sources, including the participants’ own memoirs.

Where the Conspiracy Overreaches

The more extreme versions of the dollar debasement theory — popularized by figures like G. Edward Griffin in The Creature from Jekyll Island (1994) — posit that the Federal Reserve is part of an international banking conspiracy to enslave humanity through debt. Griffin connects the Fed to broader theories about the New World Order, the Rothschild banking dynasty, and a deliberate plan to create a one-world currency and government.

These claims fail on several fronts. First, they attribute to conspiracy what is more convincingly explained by institutional incentives. The Fed does serve banking interests, but this is because it was designed and structured to include banking interests — openly, through legislation, not through secret scheming. Second, the dollar debasement narrative ignores that wages, while not keeping pace with asset prices, have risen substantially in nominal terms. A worker earning $3,000 per year in 1913 would find their equivalent today earning approximately $60,000. The system produces inflation in both prices and incomes — it just does so unevenly.

Third, the “hidden tax” framing, while useful as a rhetorical tool, obscures the fact that moderate inflation has genuine economic benefits. It reduces the real burden of debt (including mortgage and student loan payments), discourages hoarding of cash, and gives central banks room to cut interest rates during recessions. Whether these benefits outweigh the costs is a legitimate policy debate, not a conspiracy.

The Strongest Case for Concern

The most compelling version of the dollar debasement argument is not that a secret cabal is destroying the currency for nefarious purposes. It is that the Federal Reserve has structural incentives to prioritize the interests of the financial sector over the general public, that these incentives have produced policies (particularly QE) with significant redistributive consequences, and that the Fed operates with insufficient democratic accountability for an institution wielding such enormous power.

This is the argument made not by fringe figures but by establishment critics like former FDIC chair Sheila Bair, former Fed official Andrew Huszar (who published a Wall Street Journal op-ed titled “Confessions of a Quantitative Easer”), and economists across the political spectrum from Raghuram Rajan on the right to Joseph Stiglitz on the left.

Cultural Impact

The dollar debasement narrative has been one of the most politically productive conspiracy-adjacent theories of the 21st century. Ron Paul’s 2008 and 2012 presidential campaigns brought Austrian economic critiques of central banking into mainstream political discourse, energizing a generation of libertarians and helping catalyze the Tea Party movement. His book End the Fed (2009) became a New York Times bestseller. The phrase “End the Fed” became a protest chant, a bumper sticker, and eventually a mainstream Republican position — or at least a mainstream Republican applause line.

The narrative also fueled the rise of cryptocurrency. Satoshi Nakamoto’s 2008 Bitcoin white paper was, at its core, a technical response to the dollar debasement thesis. Bitcoin’s fixed supply of 21 million coins was explicitly designed as the antithesis of fiat currency inflation. The genesis block of the Bitcoin blockchain contained a Times of London headline: “Chancellor on brink of second bailout for banks.” The entire cryptocurrency industry — now valued in the trillions — is, in a meaningful sense, a $2 trillion bet that the dollar debasement theorists are right.

The 2020-2022 inflation spike — which saw consumer prices rise at the fastest rate since the early 1980s, driven in part by the Fed’s massive pandemic-era money creation — gave the narrative its strongest validation in decades. “I told you so” became the unofficial motto of sound-money advocates as grocery bills surged and the purchasing power of savings visibly eroded.

On the other end of the spectrum, the narrative has been absorbed into QAnon and New World Order theories, often fused with antisemitic tropes about international banking families. This association makes the topic radioactive for many mainstream commentators, even when the underlying economic critique has genuine merit — a phenomenon that itself deserves scrutiny.

Timeline

- 1910 — Secret meeting at Jekyll Island, Georgia designs the framework for a central bank

- 1913 — Federal Reserve Act signed by President Woodrow Wilson

- 1914 — Federal Reserve System begins operations

- 1933 — FDR issues Executive Order 6102 confiscating gold; dollar devalued 41%

- 1944 — Bretton Woods establishes dollar-gold peg at $35/ounce for foreign governments

- 1965 — Silver removed from U.S. dimes and quarters

- 1971 — Nixon suspends gold convertibility; dollar becomes pure fiat currency

- 1980 — Gold reaches $850/ounce (from $35 in 1971); inflation hits 14.8%

- 1987 — Alan Greenspan becomes Fed chairman; era of activist monetary policy begins

- 1994 — G. Edward Griffin publishes The Creature from Jekyll Island

- 2002 — Ben Bernanke gives his “Helicopter Ben” speech on preventing deflation

- 2008 — Financial crisis; Fed begins QE1, purchases $1.25 trillion in mortgage-backed securities

- 2009 — Ron Paul publishes End the Fed; “Audit the Fed” bill gains momentum

- 2010-2014 — QE2 and QE3 expand Fed balance sheet to $4.5 trillion

- 2020 — COVID-19 response: Fed balance sheet expands from $4.2 trillion to $7 trillion in months

- 2021-2022 — Inflation reaches 9.1%, the highest in 40 years

- 2022 — Fed begins aggressive rate hikes; balance sheet peaks near $9 trillion

- 2024 — National debt surpasses $34 trillion; annual interest payments exceed $1 trillion

Sources & Further Reading

- Griffin, G. Edward. The Creature from Jekyll Island: A Second Look at the Federal Reserve. American Media, 1994

- Paul, Ron. End the Fed. Grand Central Publishing, 2009

- Rothbard, Murray N. The Case Against the Fed. Ludwig von Mises Institute, 1994

- Friedman, Milton and Anna Jacobson Schwartz. A Monetary History of the United States, 1867-1960. Princeton University Press, 1963

- Bernanke, Ben S. The Courage to Act: A Memoir of a Crisis and Its Aftermath. W.W. Norton, 2015

- Huszar, Andrew. “Confessions of a Quantitative Easer.” The Wall Street Journal, November 11, 2013

- Stiglitz, Joseph E. “The Fed’s Quantitative Easing Mainly Helped the Rich.” Vanity Fair, 2015

- Vanderlip, Frank A. “From Farm Boy to Financier.” The Saturday Evening Post, February 9, 1935

- Bank of England. “The Distributional Effects of Asset Purchases.” Quarterly Bulletin, 2012 Q3

- Cantillon, Richard. Essai sur la Nature du Commerce en Général. 1755

Related Theories

- End the Fed Movement — the political movement to abolish the Federal Reserve

- Fort Knox Gold Missing — claims that the U.S. gold reserves no longer exist

- Gold Price Suppression Conspiracy — alleged manipulation to prop up fiat currency confidence

- Plunge Protection Team — claims of government intervention in financial markets

- Wealth Inequality Conspiracy — broader theories about deliberate economic stratification

- New World Order — the umbrella theory connecting central banking to global governance

Frequently Asked Questions

Has the U.S. dollar really lost 96% of its purchasing power?

Is inflation the same as a tax?

Was the Federal Reserve created in secret?

Does the Federal Reserve print money to benefit Wall Street?

Infographic

Share this visual summary. Right-click to save.